Innovating for green gold

‘Levelling up needs to begin by improving economic dynamism and innovation to drive growth across the whole country’ (LU White Paper 2022). How much are the regions set for the green innovation boom?

‘Each local area has its own distinctive strengths and different ways to capitalise on the opportunities created by greener growth, emerging technologies, and new global markets’.

Source: Statutory Guidance for the Development of a Local Skills Improvement Plan, DfE, Oct 2022

We have written frequently on The Green Edge on the green skills being identified in many, if not all, of the English LSIPs. Indeed, we’ve even been involved ourselves in part of this work, in our offshore wind skills study for the Cumbria LSIP. But when we see the much-anticipated publication of the thirty-eight LSIPs themselves, hopefully in just a few weeks’ time, it’s important to recognise that these will cover the entire skills improvement needs – green, greening or otherwise – of each area.

We’ve been asking ourselves recently to what extent the LSIPs will factor in additionality – truly new skills and jobs, rather than skilled people crossing over from, say, ‘non-green’ jobs to a ‘green’ jobs, or perhaps through a more organic building of skills within existing jobs. Of particular interest to us in this post are those areas where government professes high ‘ambitions’, such as leveraging innovation skill pools towards the pots of gold that seem to be amassing for first-movers in the world of green technology, like CCUS.

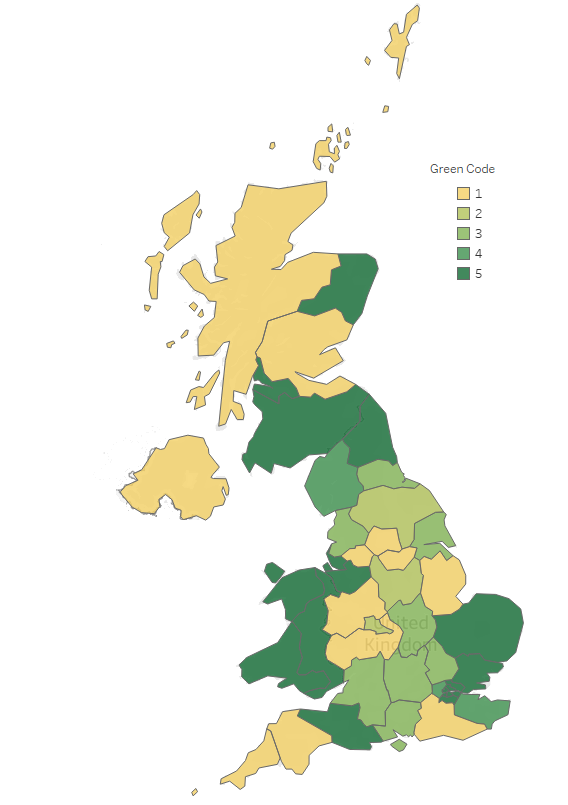

In 2022, a somewhat obscure piece of European research published in the Journal of Technological Transfer concluded, at the NUTS 2 level at least, ‘[r]egions that are already patenting in complex non-green technologies may have a comparative advantage for developing more complex green technologies’. By mapping innovative activities and technological capabilities, then cross-referencing against each region’s capacity to develop future green technologies, the research came up with simple 1 (low) to 5 (high) index of each region’s ‘green innovation potential’. The UK map looks something like this…

The Greener the Better. Image: TGE adapted from JTT.

All around the UK, every region and place is aiming to build its stock of creative, innovative businesses. Allied to this is the desire to level up and to maximise the impact of net zero investments and the transition to a carbon neutral economy. In that context, it’s interesting to look at the above piece of work, which was created in the wake of the European Green Deal and read its key findings which…

‘…suggest that green technologies, usually more novel and impactful than other technologies, require capabilities that are unevenly diffused across regions.

‘In other words, developing non-green technologies may require know-how, skills, resources that can be also useful for green technologies - and vice versa’.

Source: JTT

A little obvious, perhaps, but we think it’s important to take on board, for the following reasons:

In innovation, some regions are more equal than others

Developing local green skills plans means taking balanced views of the potential for creating and improving green technologies, and the interplay between the skills for developing both green and non-green technologies.

Before undertaking a standard skills demand-supply analysis, it’s worth digging into the innovative capacity of the region under study. We’ve seen many such studies of innovation clusters, several of which are specifically green, like those for offshore wind capabilities in Denmark and for the Greater Boston region with its five innovation ecosystems.

Productivity and innovation tend to go hand-in-hand

A key success factor of any business is the extent to which it is able to improve its productivity and incorporate new and existing technologies. There’s plenty of research out there showing clear relationships between productivity competences and those for innovation.

Local policy helps

How can local government actions support the development of skills for innovation, both green and non-green?

For example, how can local procurement policies be used to drive both innovation and Net Zero? How can the new Freeports help? Likewise, the landing of major national projects like hydrogen, CCUS, energy storage and so on?

Green is complex

We think it’s a good thing when complexity analysis is included in an assessment of a region’s growth potential. This has been tried and tested in Europe; it provides ways of viewing skills as a pool rather than through narrow sectoral ways. Several such studies in the UK are underway and we look forward to seeing the outputs during 2023.

In our minds, these questions raise the longer-term importance of the LSIPs. Above and beyond their current purpose of skills forecasting in the shorter term, we can (perhaps optimistically) see them taking on greater economic (re)generation roles in matching skills demand and supply.

We also note the recently-published Investment Zones policy prospectus, which highlights the importance of clusters and the roles of local universities. Our map below shows the specialities described by the Russell Group for their universities in proximity to the Mayoral Combined Authorities (MCAs) covered in the IZ prospectus.

Investment Zones (proposed East Midlands and North East MCA’s not shown). Image: TGE

But while City and Metro Regions seem to be well placed to take on the various levelling-up and IZ incentives, many unitary authorities may need to think a little more outside the box. Thinking of our local area here in Portsmouth: we’ve already written in past posts about the University’s collaboration with the port on green hydrogen, and Portsmouth Uni is also building a pretty handy specialism in plastics. Then we have the influence of the freeports, of which Solent has declared a goal of being a green innovation hub, as well as the Royal Navy and a raft of historically innovative businesses like IBM, Lockheed Martin, Royal Navy, Honeywell, Estee Lauder, Pall and so on. Add to that a city council that – in our opinion at least – can on occasion display the odd touch of entrepreneurship, then this particular area looks like it could make its way. Others might not be so fortunate, through forces of geography and history, or lack of resources, opportunities, or gumption.

Which gets us to a final point – for this post at least – back on the LSIPs. So far, HM Gov has splashed cash to the extent of ninety-odd million pounds on building the 38 LSIPs. But what comes after they’re published? It’s almost tempting to think of LSIPs as faits accomplis in and of themselves. But the ‘P’ stands for ‘Plan’ and that’s just what they will be, and we’d be surprised if more than a few of them, in their recommendations, aren’t calling for the sort of onward investment that we saw in some of the original trailblazer LSIPs, like this one from Sussex:

Source: Sussex LSIP Trailblazer Report.